_0.png)

IRD Tax Reform

Tax Reform

Introduction

1. Tax reform program has been initiated in Myanmar from 1988 onwards and accelerated 2010 onwards.

2. With the process of transition to modern democracy, Myanmar has adopted Framework for Economic & Social Reform and Tax Reform is one of the 10 areas of reform in the country.

3. With the Public Financial Management Reform Strategy supported by World Bank and Development Partners, Internal Revenue Department commenced Tax Policy & Tax Administration Reform.

4. The goals of Tax Administration Reform are to increase Tax to GDP ratio and to change to modern tax administration.

Tax-to-GDP ration

5. Myanmar has the lowest Tax-to-GDP ration in ASEAN. The ratio is at 3 to 5pc. Thus tax system needs to be reformed.

Modern Tax Administration

6. Modern Tax Administration includes the change to the self-assessment system (SAS) from official assessment system, the change to value added tax (VAT) and specific commodity tax (SCT) from commercial tax.

7. Tax Administration in Myanmar before 2011 is characterized by

- low capacity in the tax administration

- low level of compliance in the taxpayers

- Outdated tax policies, laws and procedures

8. Thus, Internal Revenue Department sets a vision “We must be an organization that acts with integrity and is recognized internationally as a highly effective tax administration”. Internal Revenue Department also sets a mission “To make taxpayers pay tax as good citizens, by delivering quality service in order to maximize revenue for the prosperity of the people.”

9. Reform activities which are underway according to Strategic Reform Program are

a. Tax Policy Reform

b. Legal Reform

c. Administrative Reform

d. ICT Reform

- Legislative framework reform

- Enactment of Specific Goods Tax

- Drafting Tax Administration Procedure Law

- Amendment of tax laws

- Enactment of Value Added Tax

-

- Change from Tax-typed to Functional-typed organization

- Categorize taxpayer

- Large Taxpayers

- Medium Taxpayers

- Small Taxpayers

- Offices established according to the categories of taxpayers

- Large Taxpayer Office (1-4-2014)

- Medium Taxpayer Office MTO 1/2/3

- Small Taxpayer Office STO

- Modernize assessment processes

- Commencement of self-assessment system (SAS)

- Implementation of SAS to be continued in MTOs

- VAT implementation from 2016 financial year onwards

- Utilize Technology

- Change to the system which maximizes the use of information technology (IT) in place of paper based system

- Recruit a long term ICT International Expert for an integrated technology platform in IRD

- Prioritize to provide adequate computers to all staff

- Approaches to Service and Enforcement

- Establishment of Taxpayer Service Units

- Educate the taxpayers on self-assessment

- Tax Audit and Collection of taxpayer”s information

- Programs to assist in capacity building

- Establish development programs to assist in capacity building, technical and legal support and disputes resolution processes

- Develop our staff

- Provide Trainings and seek technical assistance to raise the capacity of staff

- Get technical advice from International Advisors to enable LTO work on the processes effectively

- Find approaches to provide the staff with better facilities

- Management of Reforms

- Development of governance framework

- Setting up Reform Steering Committee

- Setting up Tax Reform Program Steering Committee

- Setting up Tax Reform Project Management Unit

- Submission of Project Reports on progress

- Increase transparency and accountability

- Transparency in planning, reporting and monitoring system

- Effectiveness in internal audit function

International Assistance

10. International assistance supporting the IRD reform program - IMF, US Treasury Office of Technical Assistance (OTA) and the World Bank - provides technical assistance, assigns resident advisors, training needs and necessary funding (loan/ grant).

Large Taxpayer Office (LTO)

11. As a pilot project of tax reform program, Large Taxpayer Office is established for the largest taxpayers in Myanmar.

Purpose

12. Purpose of the establishment of LTO

- To introduce International Good Practices in Tax Administration

- To focus on majors contributors to government tax revenue

- To be a model office for IRD that orients and implements tax reform program of Internal Revenue Department (IRD)

13. What makes LTO unique-

- First reform project to implement

- First Office practicing Self-Assessment System (SAS)

- First Office using function-based system

14. Taxpayers' obligations under SAS

- Calculation of the amount of tax due using tax returns

- Timely Filing of Tax Returns

- Timely payment of tax

- Keeping books and records

15. LTO's services

- Taxpayer education

- Stakeholders meetings

- Workshops

16. Benefits

- Limited or no contact with tax offices

- Certainty of tax payment and tax planning

- Assessment is done at the time of filing

- Reduce time and cost

- Better compliance

- Improve trust between LTO and large taxpayers.

Conclusion

Reforms are significant and Internal Revenue Department has accelerated the reform program since 2013-14 financial year. In accordance with Tax Reform Strategy, reforms are to be successful in 2014-2020. The efforts of tax officials are also significant as it is seen. The contribution of the tax officials and the cooperation of taxpaying public can lead and make the successful modernized tax administration achieve soonest.

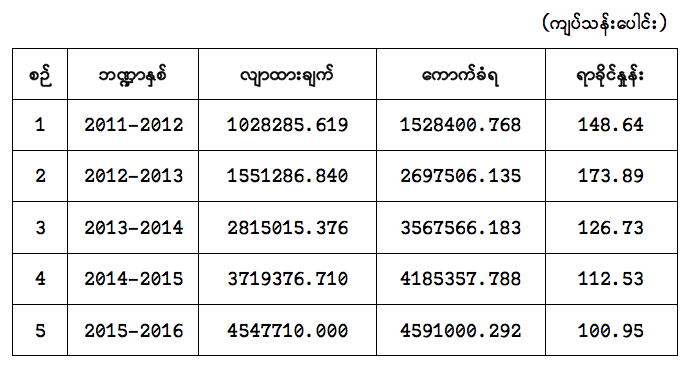

Yearly tax collection

Yearly tax collection of Internal Revenue Department from 2011/2012 financial year through 2015/2016 financial year is as below: